According to the latest Federal Reserve Survey of Consumer Finances, analyzed by DQYDJ, households headed by someone in their 60s have an average net worth of roughly **$1.7 million to $1.8 million**.

But the top 10% are in a league of their own.

To rank among the wealthiest Baby Boomers, you’ll need a net worth of at least **$3 million**. In other words, joining the financial elite of the largest and wealthiest generation in American history means becoming a multi-millionaire.

Fortunately, retirement wealth isn’t an all-or-nothing proposition. Every step toward a higher net worth can provide greater financial security, more choices, and a more comfortable retirement. And with the right investing and savings strategies, reaching that next milestone may be closer than you think.

Lawrence recently wrote in https://bestinterest.blog/dying-with-millions/

Dear Jesse,

My wife is 70 and I’m about to turn 70, and we’ve been retired for 8 years, and even with the tough market in 2022, our portfolio is up 40% from when we retired – from ~$3M to $4.2M. But I can’t bring myself to spend more…we spend exactly what we want. But I’m now wondering – what if we die with these millions, instead of putting them to some sort of good use?

Ask any retiree or any financial planner who works with retirees. Most retirees struggle to change from “saver” to “spender.” They’ve built decades of strong saving habits. Years of frugality, budgeting, and “buy and hold” investing. You can’t flip that switch overnight.

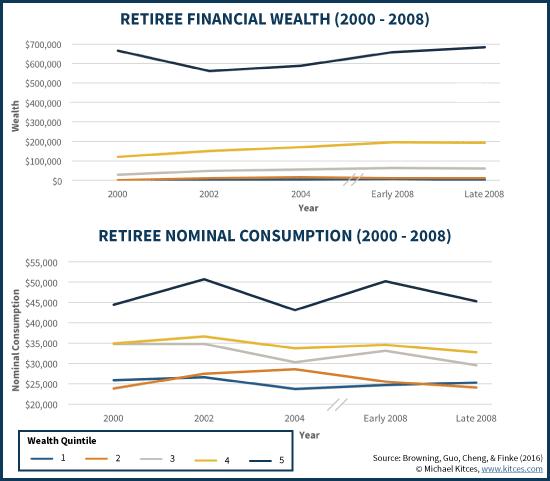

As a real example, check out the chart below. It shows retiree savings going up (surprisingly!) during the 2000s.

- My expectation was that 2000-2008 was a terrible time for retiree portfolios, considering it was the “Lost Decade” in the stock market

- But the reality is that retirees tightened their bootstraps and reduced spending during rough times, ending the 2000s with better portfolios than they started. That’s crazy!

- (Also worth noting – the bottom two quartiles (or lower 40%) of retirees have zero assets. The 3rd quartile has <$100K in assets. That’s scary and a bit sad! Save early, save often, and stay the course.)

Why is this the case? Why do portfolios tend to grow in retirement? Because most of the time, “standard” retirees and retirement planners vastly over-save.

The 4% rule, for example, was created to avoid retirement failure. Running out of money is bad. But here’s an absolutely crazy stat: the 4% rule is more likely to quintuple (or 5x) your retirement portfolio than it is to deplete it.

The required conservatism to avoid retirement failure is vital in ~5% of test cases. If you saved less, (e.g. a 5% rule, where you retired with 20x your annual spending needs), you’re more likely to fail. For better or worse, retirement planners’ first rule of thumb is the 4% rule.

Outside of the 5% failure cases, however, the 4% rule’s conservatism is overkill. Vast overkill. The kind of overkill that quintuples your money between retirement and death, and makes you realize you should have retired 5-10 years earlier.

Because that’s what we’re talking about here. Lawrence – who has lived off retirement funds for 8 years and seen his nest egg grow from $3 million to $4.2 million – probably could have retired a few years earlier. But it’s too late for that. It’s time he can’t get back.

Further reading:

Now, let’s address Lawrence’s excellent question: What if he dies with these millions, instead of putting them to good use?

- First and foremost: go work with a fiduciary CFP financial planner and (most likely) an estate attorney. You should discuss your options and preferences for this money while you live and after you pass away. How do you want your assets to positively change the world? Who is most important to you? These are the types of questions to ask and answer. Options might include: inheritances, charitable giving, ongoing endowments or trusts (e.g. “The Best Interest Scholarship”), etc.

- Don’t let society force you into spending on yourself. But if you derive joy from helping others, I’m sure there are philanthropic uses for your money while you live.

- If you have children, grandchildren, etc., remember Warren Buffett’s thoughts: leave them “enough money so that they would feel they could do anything, but not so much that they could do nothing.”

- And finally – run The McDonalds Test on your favorite things. Trust me.

One of the principle duties – albeit a “subjective” and hard-to-measure duty – of financial professionals is to imbue confidence in their clients to spend money! It’s called cashflow planning.

You should spend money. You should enjoy the fruit of your labors. Trust the math, trust the portfolio, and enjoy your life.

If you’re going to die with millions, make sure you’re putting them to good use.

Delay your retirement (if you can)

After his record-breaking career, Tucker’s contrarian view on retirement might not surprise you.

“I look upon retirement as the enemy of longevity,” he told TODAY shortly after his 100th birthday. “I think that to retire, one can face potential shriveling up and ending in a nursing home. It’s fun staying alive and working… Every day I learn something new.”

Not even the COVID-19 pandemic could stop Tucker from practicing his trade. He continued treating patients for five or six days a week during the pandemic — when his age would have classified him as high-risk.

The 100-year-old did eventually stop seeing patients in 2022, but he continued working twice a week teaching medical residents at St. Vincent Charity Medical Center in Cleveland.

While he’s acknowledged that some jobs are too physically or emotionally demanding to keep into old age, Tucker thinks you should consider delaying retirement if you enjoy your career and are still able to work.

“I’m going to caution (people): If they retire from their work, they should at least do something as a hobby, whether it be communal work or self-hobbies… you need a stimulus for the brain daily,” he said.

There can also be some financial benefits to delaying your retirement — even by just a few years.

Only 24% of Americans nearing retirement age (60-67 years old) believe they have enough money saved to live out their golden years in comfort, the Schroders 2023 U.S. Retirement Survey revealed.

A few extra years of saving and strategizing with the help of a financial planner can make all the difference and help to ease any money concerns you may have in later life.

Also, if you wait until age 70 to start claiming your Social Security benefits, you will get a much bigger payout than if you claim at the earliest possible age.

Stay fit and healthy

Tucker is a sprightly centenarian who likes to keep busy — both physically and mentally.

He’s never smoked, he has a healthy diet — thanks to his “excellent chef” of a wife, who includes greens with every meal — and he drinks alcohol in moderation, allowing himself the occasional martini.

To this day, Tucker loves to exercise.

“Swimming, jogging, hiking, and skiing well into my late-80s has kept me strong and healthy,” he wrote in an article for CNBC.

In his 11th decade, while he’s “not quite as active as [he] once was,” Tucker still claims to go at least three miles on his treadmill “at a brisk pace” most days a week — with the help of Turner Classic Movies to overcome boredom.

He’s also taken up snowshoeing after his family banned him from skiing in his late 80s following an accident.

Staying fit and healthy into your later years can come with its financial advantages. For instance, you might be able to shop around and find cheaper health insurance to cover unexpected health emergencies — which no one is immune to, even those with lucky genes.

Learn something new every day

Upon receiving his Guinness World Record in 2021, Tucker said: “I would tell my teenage self to learn each day as if I were to live forever, and to live each day as if I were to die tomorrow.”

Tucker has practiced this philosophy for decades. To this day, he keeps on top of the latest advancements in neurology by studying and reading.

And he didn’t stop at medicine. He went to law school at night in his 60s and passed the Ohio Bar Exam at age 67 — while doing his normal doctor’s day job — simply because he was interested in the law.

More recently, this love of learning has seen Tucker getting help from one of his 10 grandchildren to understand new technology and apps.

“The whole world is full of computers and they live by computers. If I want to stay in this world, I’m going to do it,” he told USA Today

Invest in Index Funds

1 Warren Buffett Index Fund That Could Turn $500 per Month Into $1 Million

Provided by The Motley Fool

Warren Buffett is one of the most accomplished investors in history. His knack for evaluating businesses and picking stocks has not only made Berkshire Hathaway one of the largest companies in the world, but also helped him amass a personal fortune totaling more than $100 billion.

Those bona fides make Buffett an excellent source of inspiration, and one piece of advice stands out from the plethora of wisdom he has imparted over the years. When asked for investment ideas, Buffett has consistently recommended an S&P 500 index fund, calling it the most sensible option for most investors.

The S&P 500 provides diversified exposure to the U.S. stock market

Index funds come in countless shapes and sizes, but they all track a specific market benchmark. Some are very narrow in scope, such as artificial intelligence-focused index funds, while others are much broader. S&P 500 index funds like the Vanguard S&P 500 ETF (NYSEMKT: VOO) lean toward the broad side of the spectrum, and that breadth is important because it offsets the risk inherent to narrower portfolios.

Specifically, the Vanguard S&P 500 ETF measures the performance of 500 large-cap American businesses, inclusive of value stocks and growth stocks, from all 11 stock market sectors. It covers about 80% of the U.S. equities market and 50% of the global equities market, meaning investors get exposure to many of the most influential businesses on the planet.

The 10 largest holdings in the Vanguard S&P 500 ETF are detailed below, ranked by weighted exposure.

Apple: 7.7%

Microsoft: 6.8%

Alphabet: 3.6%

Amazon: 3.1%

Nvidia: 2.8%

Tesla: 1.9%

Meta Platforms: 1.7%

Berkshire Hathaway: 1.6%

UnitedHealth Group: 1.2%

ExxonMobil: 1.2%

Buffett sees that diversity as a compelling investment thesis. He once described the S&P 500 as a “cross-section of businesses that in aggregate are bound to do well,” and he has consistently cautioned investors not to bet against America.

The S&P 500 regularly outperforms professional money managers.

What to Invest In?

RFK explained how our corporate overlords, who control far more of the world than even the World Economic Forum’s (WEF) leadership, are attempting to purchase upwards of 60% of all U.S. single family homes by 2030.

“There are three giant corporations: BlackRock, State Street and Vanguard, which own, collectively, own each other, so it’s really one giant corporation, but they also own 89% of the S&P 500. They own everything,” RFK said.

What about Annuities for Retirement?

He says he owns his home outright, worth about $850,000 with no mortgage. He’s expecting $3,500 a month in Social Security.

And then there’s that $2 million pile.

If you’re not worried about leaving any money behind, the simplest solution is an immediate annuity — an insurance contract which converts a pile of money into a pension, by providing you with a guaranteed stream of income for life.

Immediate annuities (not to be confused with “variable annuities”) in general are a good part of a retiree’s portfolio, as they effectively help insure against outliving your money. Economists, even without prompting from the insurance industry, have tended to argue that more retirees should own them.

And this is a comparatively very good time to buy annuities — at least better than in recent years — because the annuity market is tied to the bond market. Bonds are a much better deal now than they were not long ago, and therefore annuities are too.

(Whether they get an even better deal in due course is another matter. Nobody knows.)

According to ImmediateAnnuities.com, a man of 65 with $2 million can buy a lifetime annuity right now paying a thumping $12,740 a month. Combine that with the poster’s expected Social Security, and he’s looking at an income of more than $16,000 a month, or just under $200,000 a year.

_________________________________

According to a recent report from Bloomberg, around 23 million Americans between 18 and 29 years old, roughly 45% of that age group, are currently living with their families.

“Homeownership has been one of, if not the main way that people have historically built wealth,” he said. “But now you have the killer combination of both expensive housing and high interest rates, which locks an entire segment out of the market or forces them to buy something they cannot afford.”

“You have to get better and better, or you will lose,” he said. “Try harder, work harder and you’ll do better.” And don’t forget two of Munger’s biggest tips for everyone: spend less and invest more.

Investing in Stocks the Warren Buffett Way

The notable success in that performance largely stemmed from the renowned investor Warren Buffett. Though not immune to mistakes, Buffett’s steadfast long-term strategy has proven effective. At its core, his investing philosophy revolves around acquiring quality companies at fair or undervalued prices and holding onto them for extended periods. Buffett typically grants significant autonomy to the management teams of his invested companies, intervening only when absolutely necessary. His preference leans towards businesses generating consistent cash flows, which he then reinvests into further opportunities.